Charger Aggregators and the path forward

Aggregators, CMS, eMSPs and CPOs. Will consumers ever see a unified B2C charging app? There's a poll too!

The Present

The EV revolution is well and truly underway in India. With more electric vehicles on the roads, several (50+) CPOs (Charge Point Operators) have sprung up across major highways providing services. This has created a challenging problem -- how do we decide which charger to use and for how many wallets do we need to maintain a balance? Several smart people have come up with the same solution - charger aggregators.

The biggest of all is a global charger aggregator called PlugShare. PlugShare has nearly every charger on it. Plugshare is owned by a US charging network called EVGo.

Plugshare’s biggest advantage is its comprehensive database of charging stations, which is constantly updated by users. The global EV community uses it to search for chargers and plan EV trips. The community ‘checks in’ on PlugShare and each charger has a score. This allows us to identify which chargers we can trust.

In India, PlugShare is not well known. As a result, many EV consumers do not check PlugShare to know about charger condition and state. They often rely on community inputs to plan their trips (You can check out the active Indian EV communities via my chatbot here).

This is a loss for consumers. They end up not sharing information on faulty chargers outside of their communities. Thus, many people will have a similar experience with the charger. Much of this can be avoided if people rate their experiences on PlugShare.

This allows Indian charge point aggregators (CPAs) to step up their game and disrupt the space.

The consumers want a single platform to list the location of all chargers, live status and the ability to pay via UPI / credit card. This would eliminate the need for 50 charging apps on their phones. Unfortunately, none of the apps fulfil all the above criteria.

What ails the industry?

CPOs make the heavy capex investment to build out the infrastructure. Naturally they want to ‘own’ the consumer and get all the traffic on their platforms.

It is not just that. Once CPOs start sharing live statuses of their chargers with any aggregator, CPOs expose a lot of information to competitors and close competitors. The aggregator knows the utilisation rate of each CPO on their platform. They can advise ‘preferred’ CPOs on where to and where not to set up the next charger. The aggregator can also set up chargers. This is a lose-lose situation for CPOs.

None of the aggregators have enough traffic on their apps to divert it to the CPOs. The major CPOs have higher app downloads than CPAs (Charge Point Aggregators). CPOs can’t expect new business from aggregators. Thus, CPOs have no incentive to share their information. However, would a CPO want to onboard another CPO on their platform? Highly unlikely unless they merge in the future.

Most CPOs have utilisation numbers under 10% across their entire network. Aggregators can provide additional traffic they may not otherwise receive. This puts CPOs in a tricky situation. CPOs want their network to be utilized continuously. This allows them to recoup their capital investment in the infrastructure. The additional traffic from CPAs will increase the utilization of their chargers.

There are at least seven CPAs trying to make life easier for EV consumers. Let’s look at some of them here.

What are existing players doing?

Devang Mistry, the cofounder of Pulse Energy*, says his company is a B2B SaaS platform enabling fleet operators and OEMs to offer a ubiquitous EV charging experience to their users.

To solve this problem, PulseEnergy has two apps - PulseEnergy and InstaCharge. PulseEnergy is an EV community app. It also collects chargers from various sources and lists them in this app. InstaCharge is a ubiquitous charger payment app. InstaCharge currently supports payments for ChargeZone and Bolt [select chargers] for CCS2 and Type2 connectors. They list 229 CCS2 and Type2 chargers across multiple CPOs. Since most fleet operators use DC001 and GB/T type connectors, InstaCharge has 558 of these chargers.

The community app is an excellent funnel for B2C aggregator services. Building and supporting a community also helps them understand user needs clearly.

Devang's biggest concern is not that of onboarding CPOs on his platform. He believes that fleet drivers do not like apps, so he wants to make the interface as smooth as possible for them. That is where InstaCharge comes in. Fleet operators can easily manage their fleet of cabs on InstaCharge, without worrying about charging. Cab drivers can charge their cars on this wide network with central payment systems and no OTPs. Having a wide network is particularly difficult for a single CPO to do. CPOs would need a widely spread network of chargers with many guns to make it worthwhile for a fleet operator. Aggregators have a clear winning strategy here and relatively easy and cheaper customer acquisition.

*Disclosure - I moderate the Tiago EV community on PulseEnergy.

Varun Chandran from IONAGE, in an email interaction states that they are targeting to be the go to app for all EV customers. Their 13 member team currently works with BPCL and handles listing, status and payments for BPCL.

The IonAge app lists around 856 Type2 and CCS2 chargers. However, payments and live status can be seen only for BPCL chargers.

Varun believes that supplementing CPOs with IonAge as an eMSP (eMobility Service Provider) will ensure that CPOs can remain focused on setting up the infrastructure. IonAge can help provide comprehensive and high quality customer experiences.

Charles Nadar is building an aggregator called EVJoints. EVJoints doesn’t have a public app yet nor a web interface to check out the chargers on their platform.

In an email interaction with Charles, he mentioned his ambitious goals of allowing users to book chargers and battery swapping on his platform. To get there, EVJoints would create content around their platform like articles, podcasts and videos to disseminate EV knowledge. He says that he is also focused on solving pain points for the CPOs by onboarding a charging infrastructure expert to help them with free consultations.

Among other CPAs :

Evy lists (not all) chargers from 10+ CPOs, but payment and status access is available only for 2 CPOs i.e. Electriva and ParkEV.

FastCharge as a CPA doesn’t allow charger filtering based on CPOs. A preliminary glance shows that they list chargers from many CPOs but can only receive payment for their own installed chargers.

EcoGears charger map is outdated.

Fich/Evnnovator* is an eMSP company that can help onboard other CPOs. Evnnovator has Mr. Kartikey Hariyani, Founder and CEO of ChargeZone as a director in this company. They target fleet operators to help them manage EV cab charging. From the B2C angle, I can see ChargeZone’s and Mavi Energy's chargers on their app. Mavi Energy is a charger OEM based in Pune.

* - an earlier version of this article said that Evnnovator is a company by ChargeZone. This error is regretted

Questions sent to Evy, FastCharge, EcoGears and Fich/Evnnvoator were unanswered.

From these interactions, we know that unless the CPAs can provide an increase in the utilisation rates for the CPOs, it will be difficult for CPAs to get them onboard. InstaCharge has started doing that by targeting fleet operators and providing a software stack around it to help them manage their fleets. IonAge targeted BPCL, a new entrant in the EV charging ecosystem. The B2C puzzle is yet to be solved.

How can CPAs solve B2C?

They need to take a page from Zomato’s book. Zomato had feet on the ground when it started. They scanned all the menus in a neighbourhood and put them on their app. CPAs need to do something similar. They need a person at every charger. Let’s say they are at a Statiq charger. Whenever a car comes in to charge, they should offer to pay for the charging session from CPA’s Statiq account. They should also ask the user to download their aggregator app. During a charging session, the user pays the aggregator for the session. This eliminates the need to set up a wallet.

Given the vast number of CPOs, many users may not have the CPO’s app downloaded. They can ask the consumer to download their aggregator app. Aggregators should do this exercise for a few months to understand the consumer's psyche. They’ll also understand the charger utilisation rate.

I came across a CPO assistant while I was on my Delhi journey. Even for an experienced driver like me, it was a pleasant and helpful experience. Doing this exercise for a few months will give them an idea of how to build the platform. Additionally, they can also show the CPOs that they are bringing revenue thereby winning the confidence of the CPO.

Air pollution in Indian cities is worsening day by day. Give a breathe of fresh air by reaching out to our community efforts at sarva.life

This post is supported by Sarva.

Disclosure - I am the cofounder of Sarva

What about the other players?

Google has started listing some chargers on Google Maps, but the data is incomplete. The market size in India is too small for Google to put their resources into this.

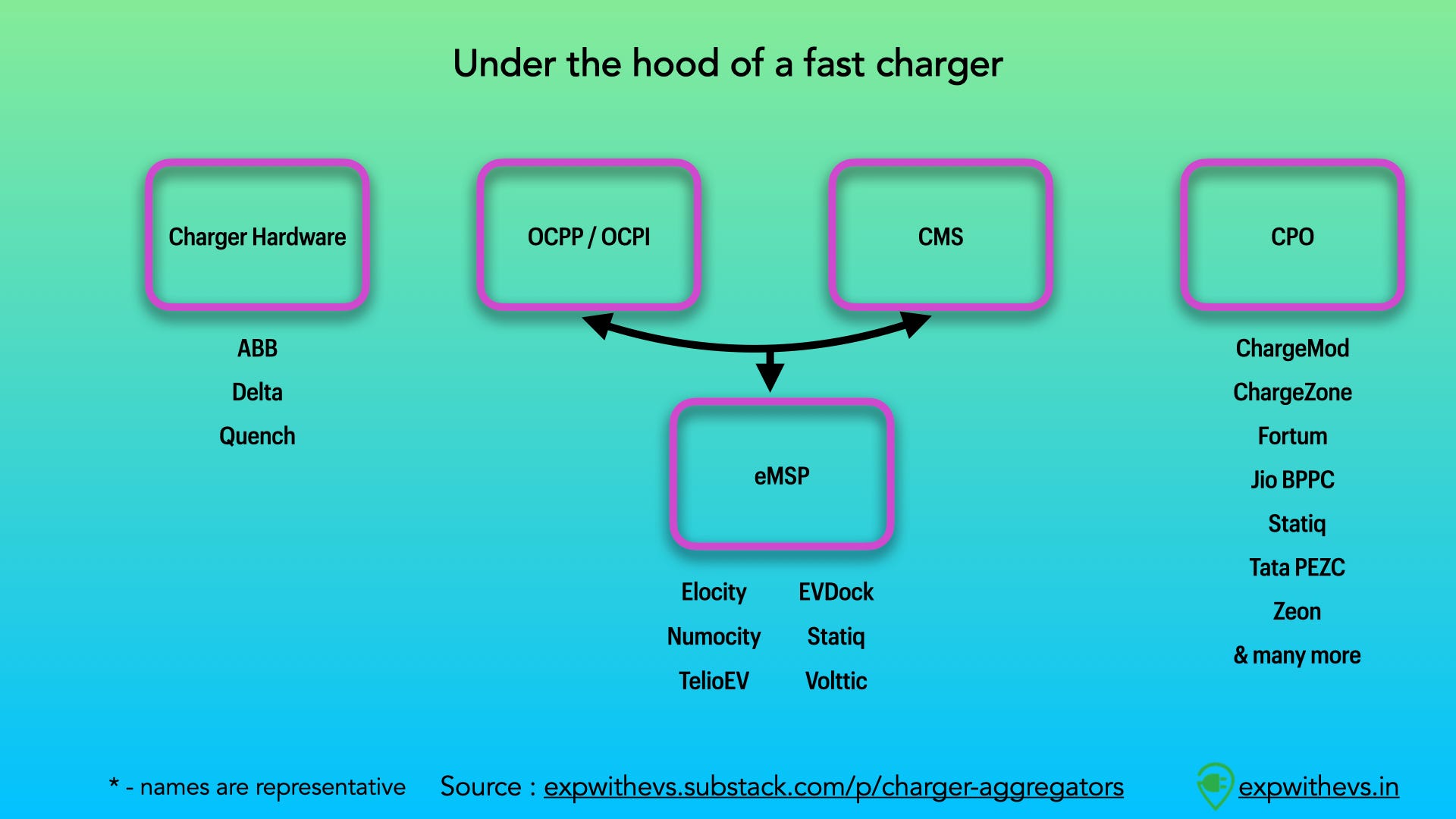

Charger hardware -> OCPP / OCPI -> CMS provider -> CPO backend -> CPO frontend. This is the stack of a typical charger. There are three players involved. The charger OEM provides the charger hardware. Then there’s a third party called eMSP (eMobility Service Provider) that uses open source protocols (OCPP / OCPI) to connect the charger to the CPO’s backend via CMS (Customer Management Service). Then there’s the CPO itself.

There are few companies in India who provide CMS and OCPP stack. The open source protocol allows interoperabilitybetween multiple charger OEMs and CPOs. This allows CPOs to switch to new hardware whenever they want. These service providers have access to real time data of the chargers, their consumption numbers and in some cases even the electricity bill that the CPO pays.

They are in a ripe position to build out a common platform charging network to absorb all CPOs. However, this would severely constrain their relationship with CPOs unless they are taken in confidence.

Alternatively, let’s say CPO A chooses a CMS and OCPP stack from the company XXCity. XXCity also serves CPO B and CPO C. XXCity can list CPO A’s charger on CPO B and CPO C’s app. Users can use their preferred app to pay for the charging session. In this case, let's say they pay using CPO C's app. The charger can be shown as busy in CPO A and CPO B’s apps.

In this case, the lion's share of the transaction would end up in CPO A’s wallet. This is because they installed the hardware and pay for electricity costs. XXCity gets their income as per their agreement with the CPOs. CPO C gets a minimal inter-usage fee for allowing CPO A to use their app. This is similar to the IUC (Interconnection usage charge) fee in telecom networks.

CPOs, CMS providers, eMSPs and CPAs should get together and figure out a solution that works for everyone! This space is super interesting and I have my popcorn ready. I’ll watch out for interesting developments!

Conclusion

Summarizing my learnings here :

CPOs are keen to share data only if utilisation rates increase. In the short term, B2B has more potential than B2C.

CPAs need to show traffic that can be passed on to CPOs.

eMSPs and XXCity are well poised to accelerate this journey.

We are still a few years away from an all-in-one app experience for B2C users.

One last thing

Thank you for reading it till the very end. Would love to know what you’d like to read more.

This piece can be re-published (CC BY-NC-SA) with a line mentioning ‘This was originally published on ExpWithEVs.in’ and a link back to this page. In case of re-publishing, please alert priyansevs@gmail.com

Text, data and graphics - Priyans Murarka

Copy editing - Siddharth Agarwal