Bull Case for Oil PSUs

Our opinion on how things can be better

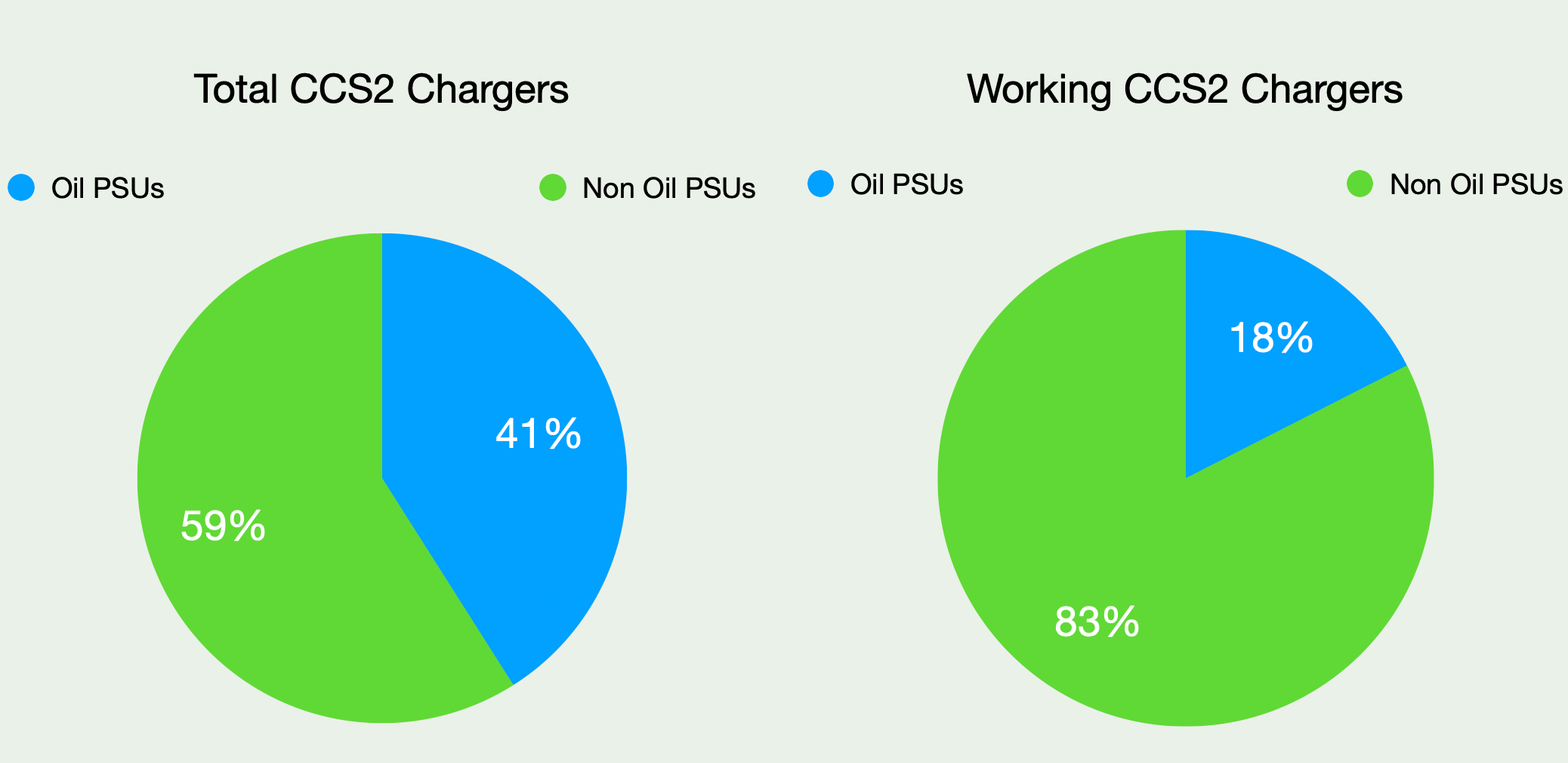

BPCL, HPCL and IOCL represent around 41% of the CCS2 charging infrastructure in India. But over various months of tracking, we’ve realised that most of these chargers are usually offline, a staggering 75% of their network is offline. Despite having such a large share of fast charging infrastructure under their network, their share in working CCS2 chargers is only 17.5%, or just under 1 charger out of every 5 fast chargers.

We look at the scenario today when these chargers are online and how it transforms electric mobility in India.

Before we get to that, here are some of the reasons why their infrastructure is not working :

Poor quality hardware

Unavailable grid demand

Poorly trained staff

Incorrect incentives and policies around chargers

Poor app experience

Let us see what is working in the Oil PSU’s favour :

Widespread infrastructure

Per kWh pricing

Subsidies to setup charging infrastructure

The bull case is dependent on increasing revenue from these chargers, which can only happen when they are online and working. In phase one, let us focus only on city chargers. We know that utilisation in cities is better than on highways. Ask any CPO and they would agree.

Our organisation is supported by readers like you. We do not rely on any promotions or advertisements by corporates or companies in the EV industry. Become a paying subscriber to help maintain our independence.

P.S. : We are going live on LinkedIn today at 4:30 PM. Do join in and ask us questions!

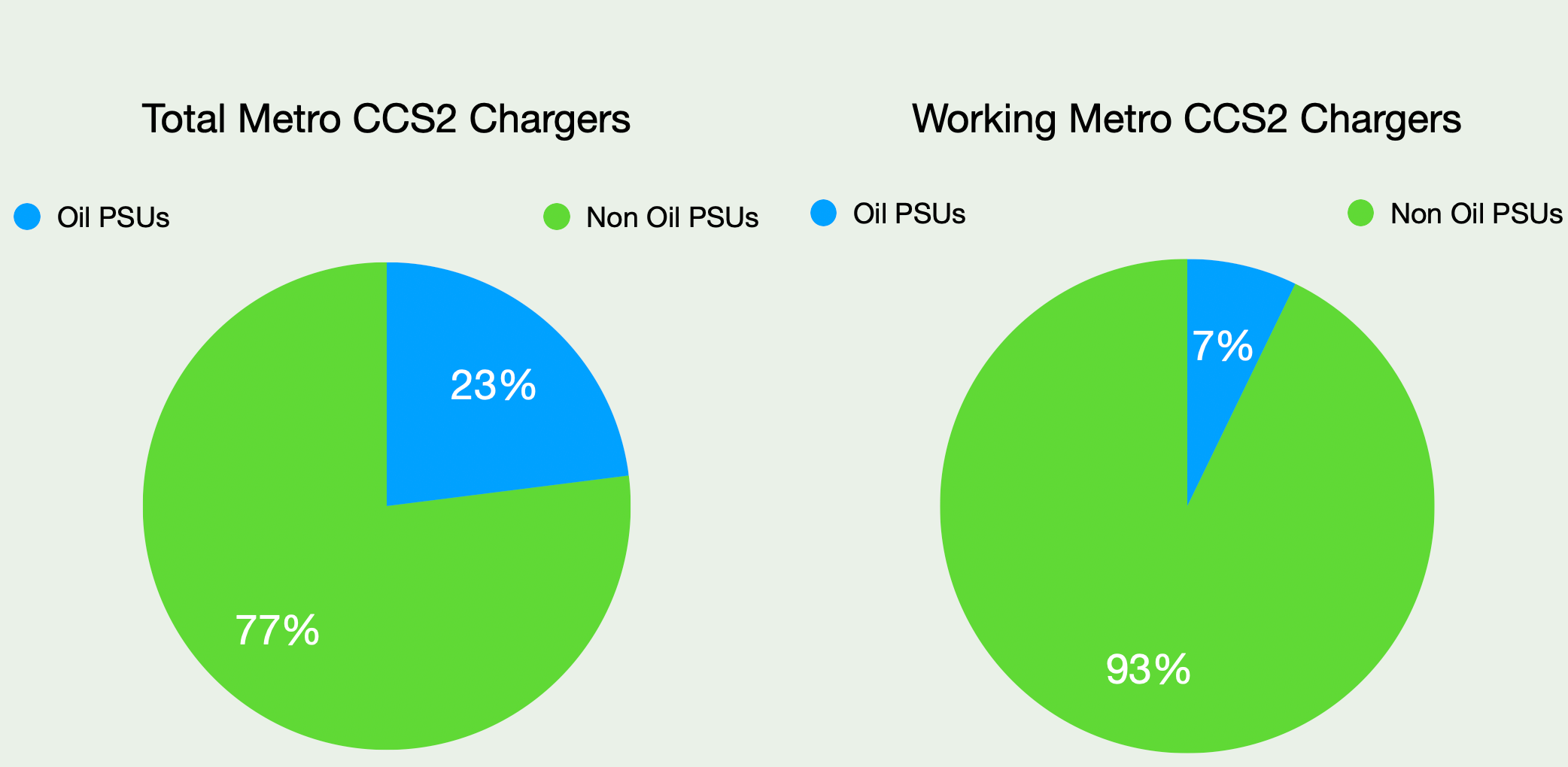

We have the data for the following cities :

Ahmedabad-Gandhinagar Bengaluru. Chandigarh Chennai Delhi NCR

Hyderabad Indore Jaipur Kochi Kolkata Kozhikode Lucknow

Mumbai MR Pune Surat Thiruvananthapuram Vadodara Visakhapatnam

Despite having one out of almost every four chargers in the above cities, Oil PSUs have been able to manage to get less than one out of ten chargers online and working.

The cost of procurement of the chargers put up by Oil PSUs is far lower than the hardware being procured by Private players. The Oil PSUs follow a tendering process and the lowest bidder (L1) gets to supply the goods. The second reason for cheaper procurement is the subsidies being given by the Central Government to Oil PSUs to setup charging infrastructure.

We do not have the data on quality of hardware being procured by the Oil PSUs, but we will assume that the hardware installed is certified and approved by the relevant authorities to charge cars.

Related reading - In July 2023, I had written an article on the state of poor EV charging infrastructure by BPCL for The Ken.

The PSUs started their journey in EV charging infrastructure with 25-30kW chargers but have now graduated to 60kW and 120kW chargers. They are leading the trends when it comes to high capacity charging infrastructure. IOCL* is a clear winner when it comes to 120kW chargers and above. No private CPO is even close to matching the coverage and scale of the Public CPOs.

I believe you have your answer to my LinkedIn poll!

They are not stopping here though. From a recent press release by Servotech :

And another one from Zetwerk :

It is a detriment to the industry if these high capacity chargers are not being put to use.

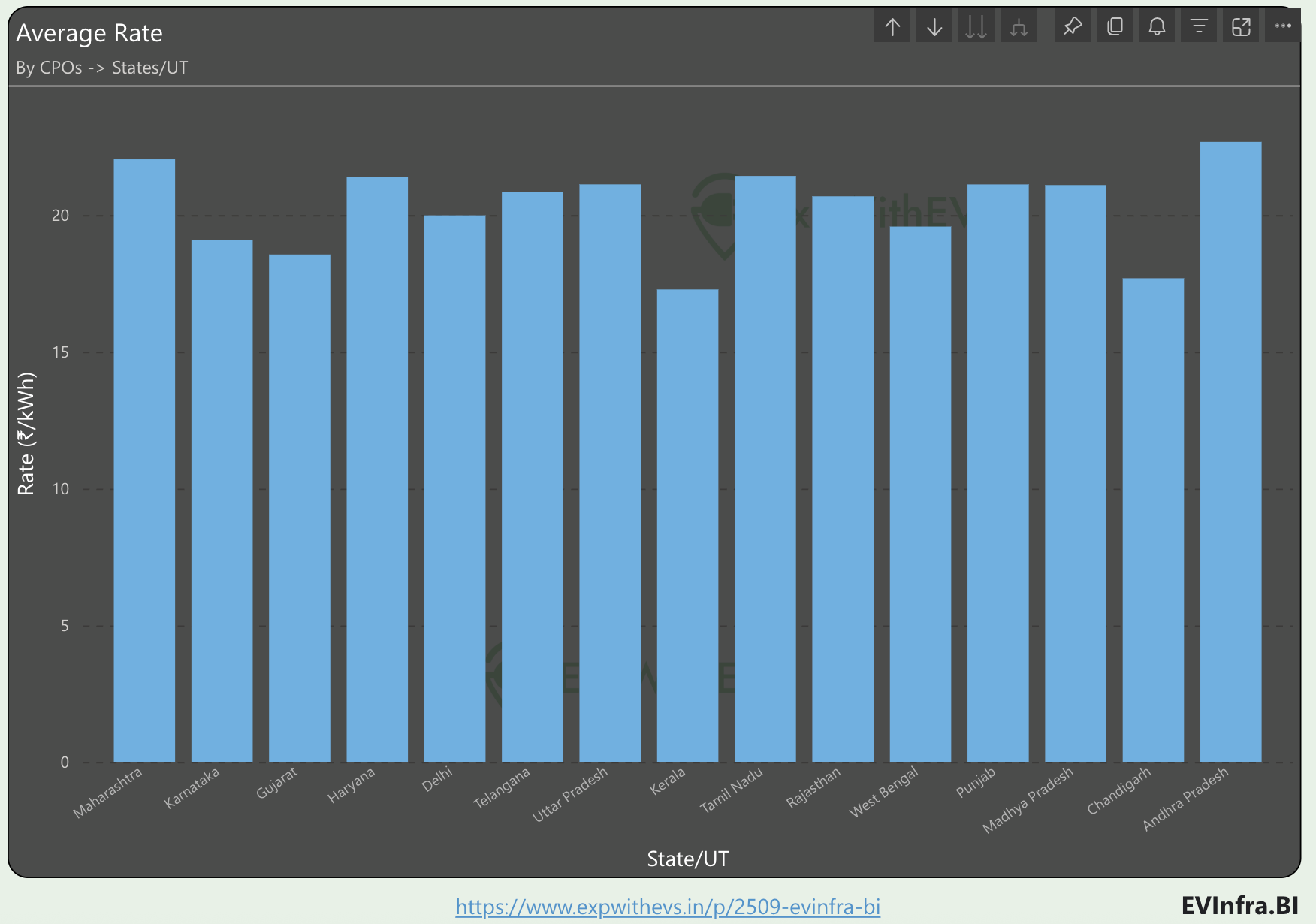

The average rate of charging in these cities for Non Oil PSU chargers is as follows

On an average, the market charges around INR 18.5 / kWh (US$0.2) when the PSUs are not included.

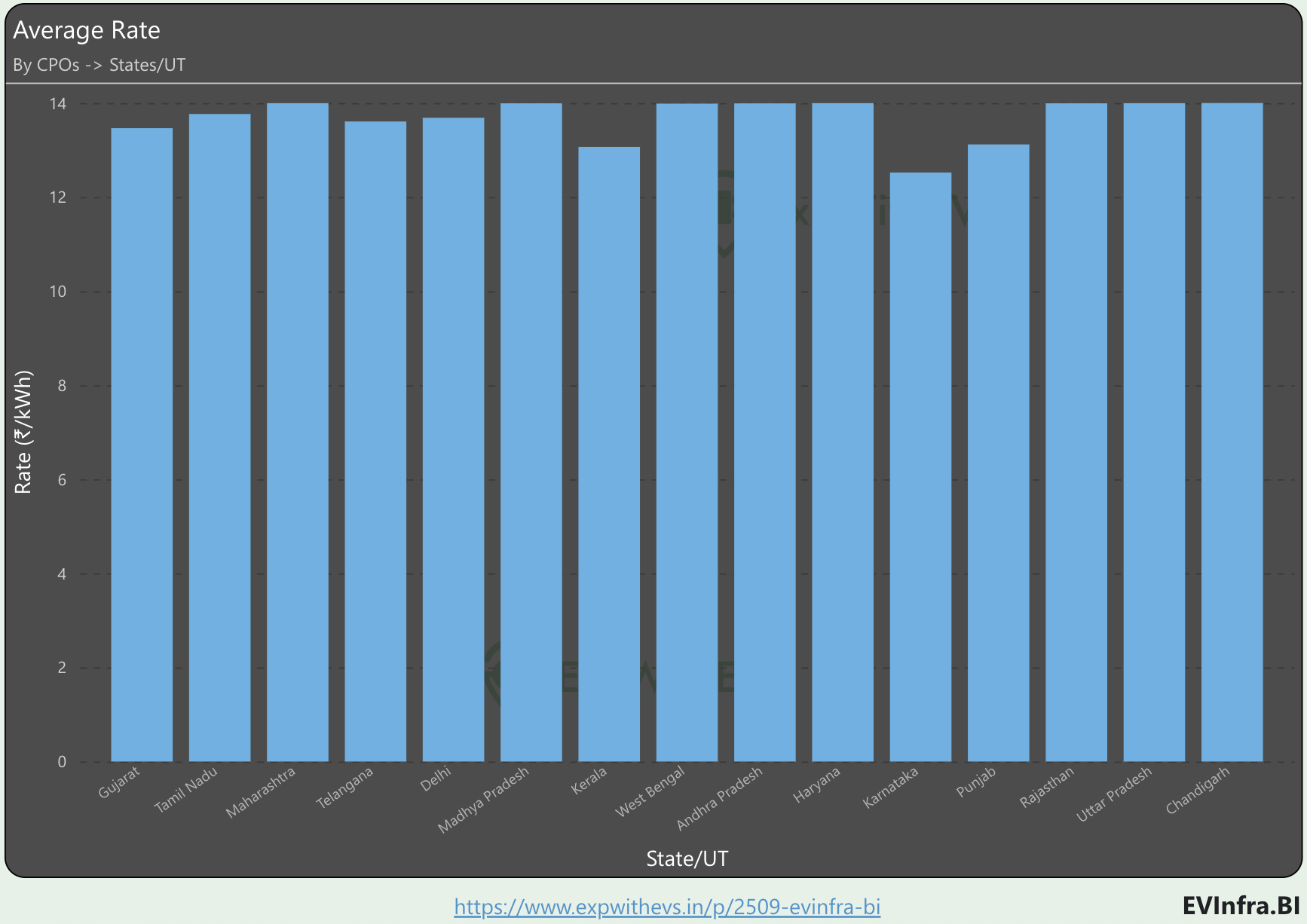

The three Oil PSUs charge roughly INR 13.5 / kWh (US$0.15) in these metro cities as seen in the chart below.

The advantage here is that when their chargers are working, it is usually the cheapest option. There are some other players like EVMithra (public) and NKDA - New Town Kolkata Development Authority (public) charging lower than the Oil PSUs, on an average. These players are restricted to Bengaluru and Kolkata respectively. Unlike the Oil PSUs.

EVMithra is run by BESCOM, Bengaluru city’s electricity board. They charge roughly INR 7 / kWh (US$0.08) which is significantly cheaper than all other players in the market.

In our premium WhatsApp community group, we discussed how difficult it is to charge on EVMithra’s network in Bengaluru. For EV community owners in Bengaluru, you already know why. Most of their charging stations are occupied by fleet cabs.

Fleet cabs are the silver bullet to push e-mobility story forward for Oil PSUs.

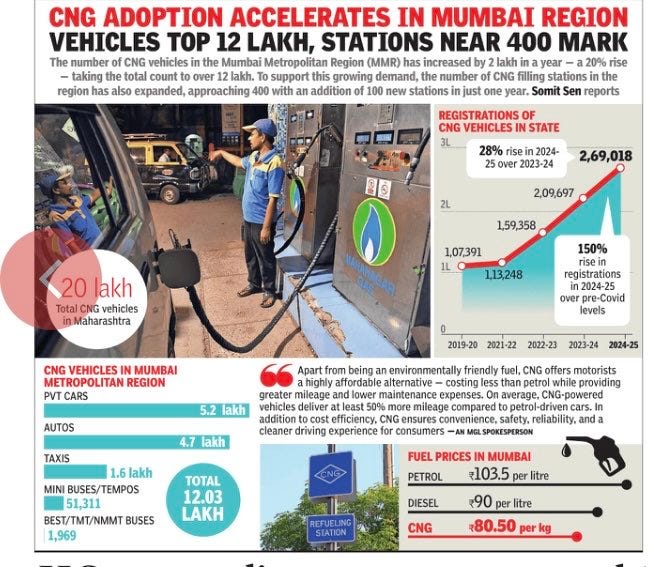

For any fleet operator, the biggest cost is the upfront CapEx, which is usually backed by loans, thus leading to recurring EMI payments. There’s driver fees and then there’s fuel, maintenance and other admin expenses. The intracity cabs are mostly in CNG in major metro cities. Next time you are visiting a CNG pump, observe the queue and count the number of cars lined up to fill in CNG.

The above image is a clipping from a recent Times Of India article, posted by Somit Sen of Times of India. 12,00,000 CNG cars for 400 CNG stations, implying 3000 cars per CNG station. This ratio is far worse than EV cars to EV Charging Stations ratio.

For any fleet operator, any marginal gain in fuel savings will result in tremendous savings as fuel forms a considerable part of the expense. From Rahul Mathur ‘s post on Twitter about erstwhile Blusmart, we see that electric cars, on an average, spend between INR 120 to INR 180 for charging per day per car. Keeping in mind that this analysis was for BluSmart and from 2023, we can assume that with slight increase in pricing, this number is closer to INR 200 on an average.

We know that operators like Blusmart have preferential pricing with large private Charge Point Operators because of demand predictability. These CPOs are private and install captive charging hubs for fleets. As we’ve seen above, the pricing by CPOs is around INR 18.5 / unit. When a fleet asks for a discount from a private CPO, their charging costs can be closer to INR 16 / unit, which translates to a saving of INR 20 - INR 30 per car per day.

If the Oil PSU chargers are working everywhere in the city, and if fleet owners move to such CPOs, then the fleet owners can save additional INR 2 / unit, translating to INR 20 to INR 30 per car per day. This is assuming that there is no bulk discount negotiation with the OMCs.

In Bengaluru’s BESCOM, the fleet operators are saving around INR 9-10 / kWh, resulting in atleast INR 120 per cab per charging session. When you have a network as wide as the PSUs or concentrated like BESCOM, then the only way to make money is through volumes. This is a low margin business but volumes make up for a healthy profit margin.

It is best interest for small fleet operators with 10 - 20 cabs to charge at PSUs. They do not have the volume to negotiate a bulk discount with private CPOs. We know that there are plenty of such small fleet operators in India.

When these chargers start working, the immediate impact will be felt on private CPOs catering exclusively to the fleet business. This will happen irrespective of PSUs because bigger CPOs - say JioBP, can drop prices to capture all the fleet volume to their charging hubs.

Location availability in cities is low than on highways. The PSUs already have the land and the infrastructure to support it. Private CPOs have to pay a premium to get land at prime locations to service business districts, airports, etc.

While in rural regions, power availability can be a bottle neck to get the Oil PSUs charging infrastructure up and ready to run, but that is not the case in urban regions. It is a function of will and the rest will follow.

Let us look at some of the other examples in our country.

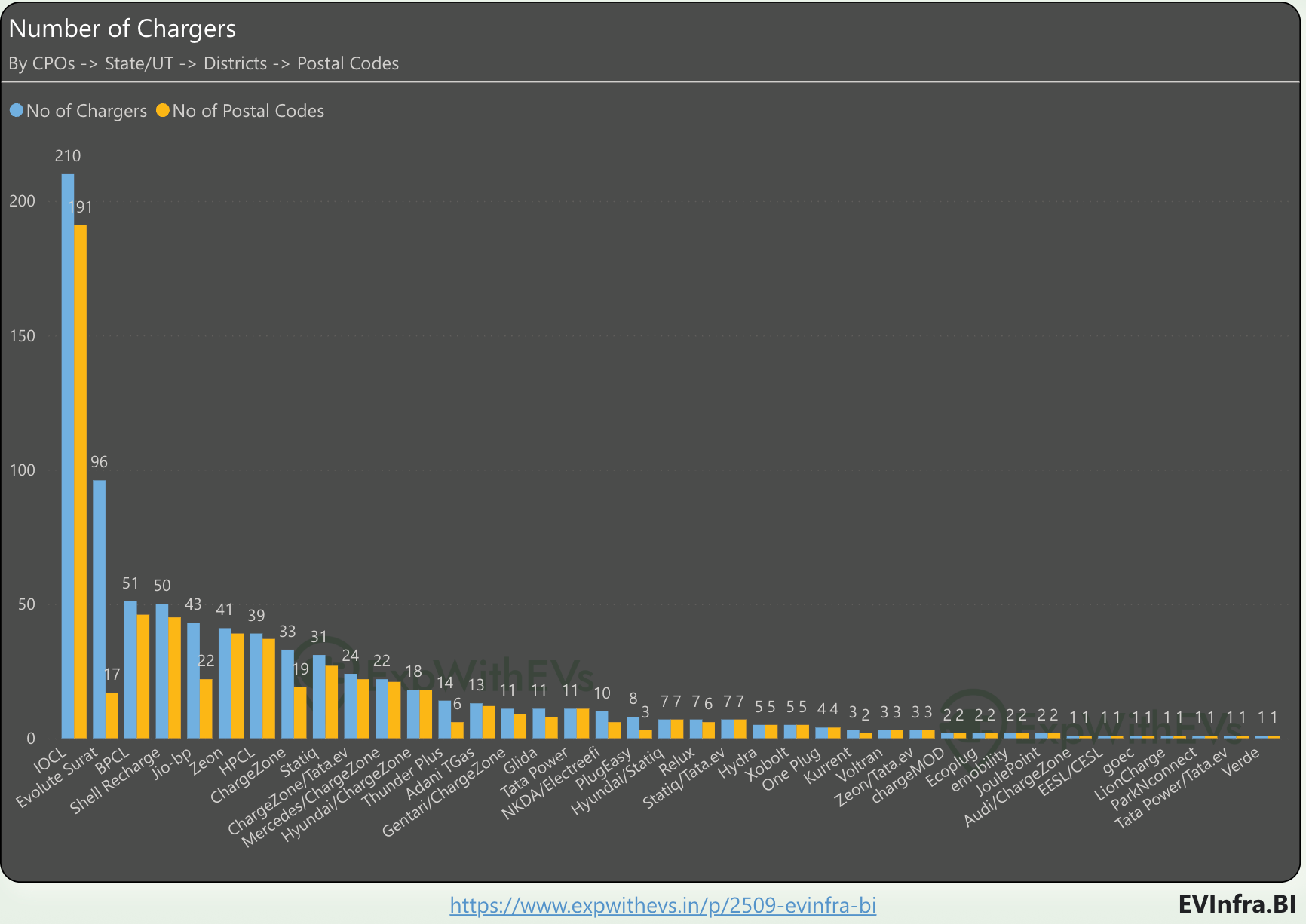

Tata Power, Shell Recharge and Jio-bp are other major players to have chargers at fuel pumps in major metro cities in India.

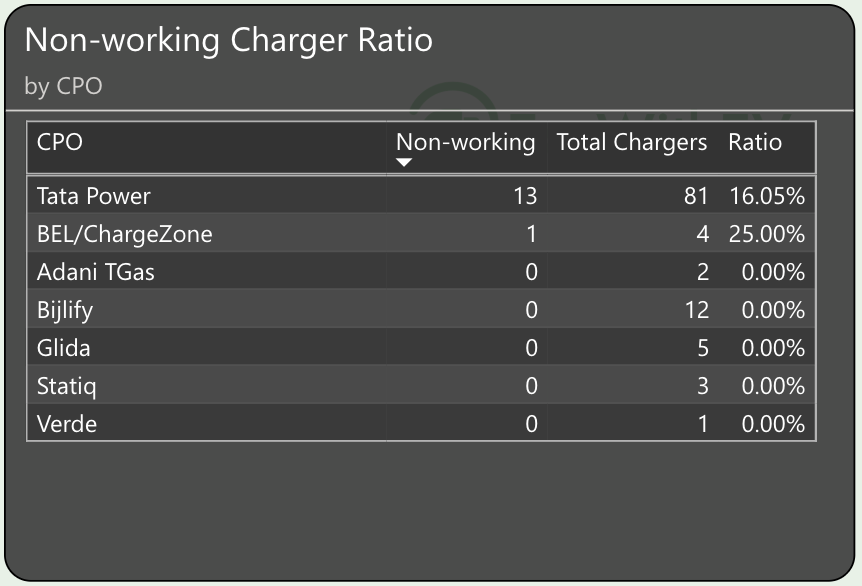

We see that there are 191 CCS2 chargers across fuel pumps in major metro cities in India.

Of these, 108 are at government fuel pumps - including those of HPCL, BPCL and IOCL. Among those 108, only 14 chargers are not working, making it only 13%, whereas the Oil PSUs are at staggering 78% non working.

One more value addition of having chargers online in cities for PSUs is to capture the carbon credit. They are in a massively polluting industry and by having working chargers, they can earn carbon credits instead of buying them.

At the Oil PSU level, they can have conversations with the State Discoms to improve the grid availability for their chargers. It is in a Discom’s best interest to have electricity available as they get captive customers. A fleet electric car can consume 300 units of electricity every month, which is equivalent to atleast two households in Delhi NCR. For the fuel pump owners, the Oil PSUs can incentivise them on volume of electricity dispensed via their chargers.

If the Oil PSUs are short staffed or believe that they do not have adequate resources to handle this new business vertical, they can always outsource the work to a big four company (like how BESCOM did) or to certain sector experts.

We hope that the Oil PSUs are looking at this opportunity closely and are willing to set the right standards at their fuel pumps, especially the ones owned and operated by them directly. The PSUs have a right to penalise the Charger OEM incase the hardware stops working within the warranty period.

Other low hanging fruit is having clean washrooms at the fuel pumps. The Oil PSUs can align the incentives to be in sync with the Prime Minister’s Swacch Bharat campaign. Having clean washrooms will not only welcome customers but also help reduce diseases among their own staff.

The grand old PSUs need to see that there’s light at the end of the tunnel, the country will transition to electric, with or without their support. They can be a part of the revolution or sit by the sidelines and become less relevant day by day while wasting public resources.

* - IOCL’s app has often been buggy and we try our best to collect data as diligently as possible.

This piece is proprietary and a property of ExpWithEVs. You may not republish, copy, edit, repost or reshare this piece without prior written confirmation from ExpWithEVs via email : priyans@expwithevs.in