ASEAN’s EV Surge: Why India Risks Being Left Behind

Singapore is at 34% EV adoption, Thailand has already beaten its infra targets, and Vietnam’s VinFast is scaling globally. What can India learn and what happens if we don’t?

This is a part two of Hong Kong series of articles. You can refer to Part One here, where we talk about our observations about electrification in Hong Kong.

When we talk about EV adoption, India often looks at Europe, the U.S., even China. But the real story might be unfolding closer to home. With over 600 million people and a combined GDP similar to India’s, ASEAN is already a global auto manufacturing hub. What happens here will shape EV supply chains, investments, and consumer adoption across the Global South.

Big picture

Singapore has hit 34% EV adoption in 2024, and plans to phase out ICE cars entirely by 2030.

Thailand already surpassed its 2025 charging infrastructure target two years early, and has pulled in billions in EV manufacturing investments.

Vietnam has turned VinFast into ASEAN’s second largest EV brand after BYD, scaling production from 97,000 units in 2024 toward half a million by 2028.

Beyond the big three, ASEAN is also experimenting with models that India has debated but not yet uniformly acted upon. The Philippines already operates nearly 500 battery swapping stations, while Indonesia is targeting 15 million EVs by 2030 — most of them scooters.

ASEAN is a live test bed of what works and what doesn’t in emerging markets. Whether it’s battery swapping in the Philippines, OMC-led charging rollouts in Thailand, or policy-driven adoption surges in Singapore and Vietnam — the region offers a set of experiments India can’t afford to ignore. India is still hovering around 4-5% EV sales for cars, with no ICE sunset date and patchy infra growth.

In our today’s article, we cover the following :

Country by country breakdown : Adoption trends, infra targets, manufacturing investments across Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines, and more.

Cross cutting insights : 2W vs 4W adoption, charging business models, manufacturing bets, policy experiments.

Implications for India : Where India is ahead, where it is already falling behind, and what lessons policymakers and industry leaders need to act on today.

Acknowledgements

The insights in this article draw heavily from presentations and discussions at The Battery Show Asia (Hong Kong), alongside public datasets and industry sources across ASEAN.

Special thanks to Dr. Yossapong Laoonual, Prof. Evvy Kartini, Dr. Sing Yang Chiam, Nguyen Quang Minh, Andre Luis D. Reyes, Edmund Araga, and many others who generously shared their research, on-ground experience, and perspectives over discussions at the event. Their inputs were invaluable in shaping this ASEAN EV Outlook. I strongly recommend visiting the Battery Show Asia next March to get a deep understanding of the ASEAN and China market.

Special thanks to Jaan for preparing a global overview of EV sales at EVWire.com. Subscribe to support him.

Community updates

EV Jobs Matching Form

Looking to work in EV charging infrastructure, or hire talent in the sector? I’ve created a form to connect candidates with employers. It’s free for candidates.

CXO Road Trip: Delhi → Bengaluru

Final call for CXOs who’d like to join me on an EV road trip early September. The idea is to experience first-hand what EV drivers go through when planning and charging on India’s highways. Drop me a message and we will figure out the logistics.

Psst. I am looking for places to host an industry meetup in Hyderabad and Bengaluru in September. If you have suggestions, please let me know!

Charger Utilization Report

Our latest report on charger utilization is now live — covering national averages, metro vs. highway trends, and downtime patterns.

The Leaders: Singapore, Thailand, Vietnam

🇸🇬 Singapore

Singapore isn’t just another ASEAN market. It is the only “developed” economy in the region, with a highly educated population, strict governance, and a track record of hitting policy targets with discipline. EV share of new car sales surged from 6.5% in 2022 to 34% in 2024. The plan is clear: 100% clean new car sales by 2030, with rebates of up to SGD 25,000 (USD 19,000) and penalties for ICE owners.

With 60,000 chargers planned and EV-ready housing estates, Singapore shows that in the right conditions — educated consumers, high governance capacity, and urban density — EV adoption can move from single digits to a third of sales in just three years. The numbers don’t just prove ambition; they prove that Singapore lives up to its reputation as ASEAN’s only truly developed market.

🇹🇭 Thailand

Thailand’s EV story isn’t an overnight success. The country has long positioned itself as the automotive hub of Southeast Asia, supplying cars and parts to the region for decades. That industrial base — combined with infrastructure planning and incentives — means the EV shift is building on existing strength.

Some of this momentum reflects a “China+1” strategy — global OEMs like BYD and Changan see Thailand as a hedge against over-dependence on China. But equally, Thailand itself laid the groundwork early: policies to attract foreign direct investment, industrial clusters for auto parts, and a strong logistics backbone. Today, with over 6,100 DC chargers already installed and car adoption hitting 14% by mid-2025, Thailand is turning those foundations into EV leadership.

The country isn’t just following China’s lead — it has earned its place as ASEAN’s EV Detroit through decades of industrial policy discipline.

If you’ve been tracking Thailand EV sales, then you’d observe that year on year growth has declined by ~10%. Jaan clarifies this in his newsletter.

Thailand would look like a declining EV market here… if you don’t have the context. You see, Thailand was the #2 in EV growth globally in 2023, growing 705%! Repeating that seems pretty impossible so a slight YoY decrease is almost expected, but notably the EV market share remained pretty much the same (12.33% in 2023)!

(Numbers might be slightly different)

🇻🇳 Vietnam

Vietnam’s EV success revolves around VinFast, a domestic national champion backed by both state support and export ambitions. VinFast has opened its first few dealership stores in India and USA. In 2024, EV share of new car sales reached 23%, with VinFast producing nearly 100,000 vehicles and targeting half a million by 2028.

This is not a coincidence. Vietnam, like China, is a communist state with a capitalist bent, where governments promote national champions as the vehicle for industrial policy. Just as China nurtured BYD and CATL, Vietnam is elevating VinFast to be its flagbearer — at home and abroad.

The model has risks — concentration around a single company, dependence on state support, exposure to global market acceptance. But the results are undeniable: in less than a decade, Vietnam has gone from zero to being one of ASEAN’s EV leaders.

Michael Dunne newsletter recently covered the rise of Vinfast in his newsletter here.

Takeaway from the Leaders

Singapore shows how policy alignment in a developed economy accelerates adoption.

Thailand demonstrates that decades of groundwork in automotive manufacturing can be leveraged for EV leadership.

Vietnam illustrates how political systems that promote national champions can create rapid momentum.

Together, they form the three pillars of ASEAN EV leadership, each with a distinct playbook.

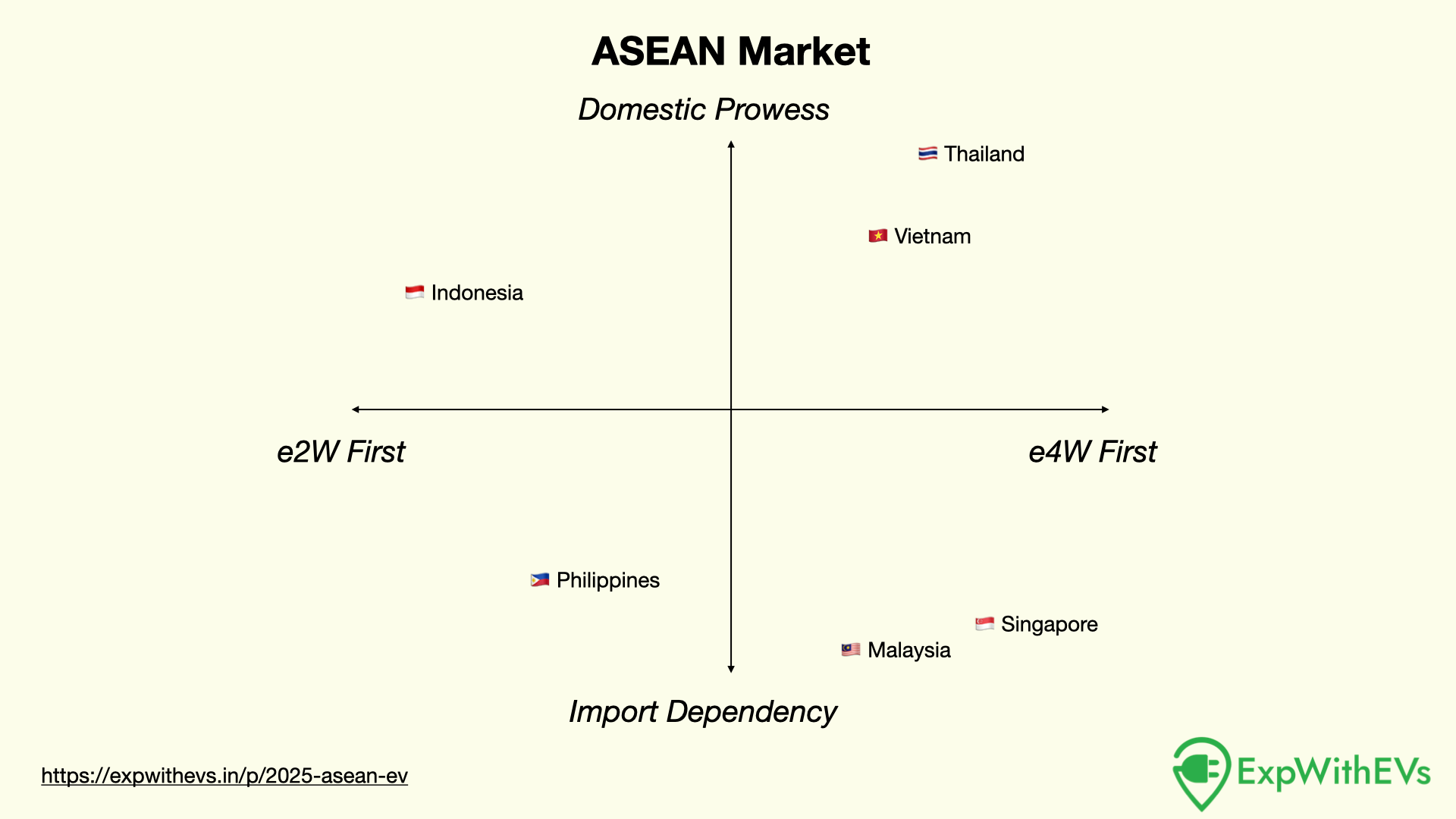

The challengers: Indonesia, Malaysia and Philippines

🇮🇩 Indonesia

Indonesia is betting on two-wheelers first — a logical move in a country where motorbikes dominate daily life. Its target of 15 million EVs by 2030 (13 million scooters) reflects a mass-market strategy.

The bigger story is Indonesia’s resource nationalism. Sitting on the world’s largest nickel reserves, it has banned raw ore exports and is forcing battery companies to process and invest locally. Nickel is key because it enables higher-density battery packs — critical for scaling EV adoption beyond just scooters.

At the same time, two-wheelers are a natural entry point: they require smaller battery packs, which are a low-hanging fruit for new factories being set up in Indonesia. Manufacturers can scale up production of smaller packs first, while building capacity and expertise for larger, higher-density EV batteries down the line.

This dual advantage — abundant nickel for high-density packs, and mass adoption potential through e2Ws — makes Indonesia’s play uniquely compelling. The state isn’t just driving consumer adoption; it’s using its resources to shape the EV supply chain from the ground up.

🇲🇾 Malaysia

Malaysia’s EV adoption (~20% of annual car sales in 2024) looks strong on paper, helped by tax and road fee exemptions. But beneath that, the industrial depth is thin.

Unlike Thailand or Vietnam, Malaysia lacks a strong battery or EV manufacturing anchor. Chargers are being rolled out (10,000 targeted by 2025, with one every 60 km on highways), but there is no equivalent push to localize cells, packs, or OEM assembly lines.

This leaves Malaysia vulnerable to becoming an import-dependent EV market. Adoption may grow, but the real value capture — manufacturing, exports, and technology — remains abroad.

Without a domestic anchor industry, Malaysia risks becoming a pass-through market: good adoption, weak industrial dividends.

This news came in two days ago, where BYD is planning to setup a CKD manufacturing unit in Malaysia. Things might be changing for Malaysia?

🇵🇭 Philippines

The Philippines is unusual: nearly half of its 1,100 charging points are battery swapping stations, despite higher costs (~USD 0.94/kWh vs 0.60/kWh for DC).

The reason it works is urban design. Metro Manila and other large cities are dense, traffic-heavy, and fleet-dependent (taxis, jeepneys, delivery 2Ws). Swapping offers a fast turnaround in contexts where downtime kills productivity.

By legislating charging mandates at gasoline stations (through the EVIDA Act), the Philippines is forcing infra into place. While costs are high today, localizing swap battery manufacturing could reduce dependence on imports and improve economics over time.

Swapping aligns with the Philippines’ density + fleet-heavy transport system, making it a viable policy experiment even if costlier per kWh.

Takeaway from the Challengers

Indonesia → EV adoption through resource leverage and two-wheeler scale.

Malaysia → Consumer incentives without industrial backbone.

Philippines → Regulatory boldness, using mandates and swapping to force adoption.

These are incomplete strategies compared to the Leaders, but they show ASEAN’s diversity: not every country can lead, yet each is running real-world experiments that India can learn from.

The Late Movers

🇰🇭 Cambodia

Target: 30,000 EVs by 2030. Longer-term: 40% cars & buses, 70% 2Ws electrified by 2050. Adoption today is negligible, and while policy intent is visible, the market is too small to shape regional supply chains.

🇱🇦 Laos

Target: 1% EV fleet by 2025, rising to 30% by 2030. The ambition is notable, but without industrial anchors or infra buildout, it remains aspirational.

🇧🇳 Brunei

Target: 60% EV sales by 2035. As a small, oil-rich economy, Brunei’s transition is more symbolic than material — its market size means global impact will remain limited.

Takeaway from the Late Movers

Cambodia, Laos, and Brunei are policy intent markets. They align with global climate goals, but will not materially influence ASEAN’s EV industrial or adoption trajectory in the coming decade.

Cross-Cutting Themes

Two-Wheelers vs. Cars

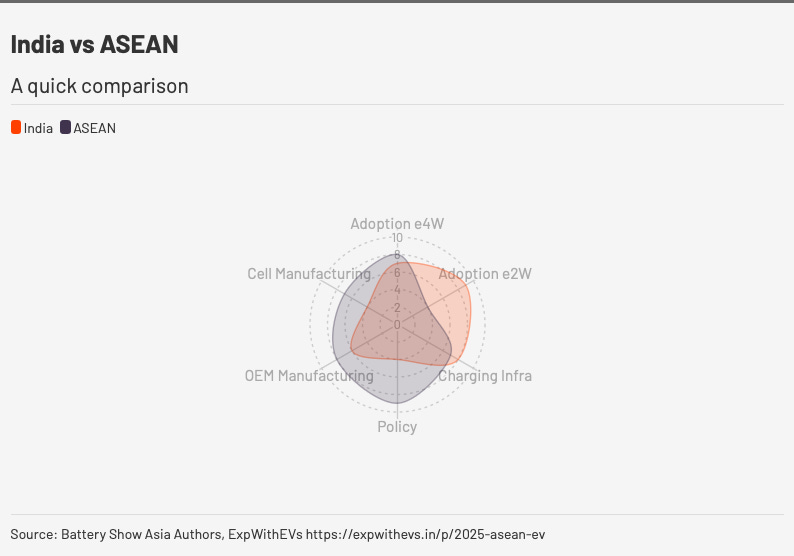

ASEAN proves there is no single EV pathway. Indonesia and the Philippines are betting on 2W electrification first, while Singapore, Thailand, and Vietnam are scaling cars and SUVs through policy and industrial push. India should take note: success in the EV transition demands serving both the scooter commuter and the urban car buyer. For context, India’s e2W adoption is under 8% and e4W is under 6%.

Infrastructure Pathways

Thailand and Singapore show that clear targets + execution can deliver infra ahead of schedule. The Philippines is bold enough to push swapping, while Malaysia mandates coverage along highways. The lesson: there is no “perfect model” — only context-driven approaches. India doesn’t need to copy-paste, but it must stop debating and start executing.

Manufacturing Hotspots

Thailand and Vietnam are pulling in billions of dollars of OEM investments. Indonesia is leveraging nickel to anchor the battery supply chain. Together, these three are shaping ASEAN as a future EV export hub. India risks being bypassed if it doesn’t match policy clarity and industrial incentives.

Policy Models

ASEAN showcases a policy laboratory:

🇸🇬 Singapore → carrots & sticks to change consumer behavior.

🇹🇭 Thailand → investment-driven, infra + OEMs.

🇻🇳 Vietnam → national champion.

🇵🇭 Philippines → mandates + swapping.

Each has trade-offs, but together they offer a menu of experiments the world — and India — can learn from.

ASEAN isn’t waiting. It is trying multiple pathways at once, while India is still debating the basics.

Implications for India

Where India Risks Falling Behind

Policy clarity: ASEAN nations are declaring phase-out dates (Singapore 2030, Thailand 2035, Indonesia 2050). India has none.

Manufacturing: Thailand and Vietnam are attracting global OEMs, while India’s footprint remains fragmented.

Infrastructure: ASEAN infra is already ahead of schedule. India’s remain patchy and unreliable.

Experimentation: The Philippines is running swapping pilots at scale. India continues to debate.

Where India Is Shining

2W adoption: India leads globally in electric scooters and bikes.

Innovation ecosystem: Startups in charging, swapping, and software are building unique solutions.

Policy intent: FAME, state subsidies, and PLI aren’t perfect, but they show India is steering.

Opportunities to Leapfrog

OEM magnetism: Replicate Thailand’s play by offering certainty to global brands.

National champion model: Back an Indian OEM (Tata.ev, Mahindra) to play VinFast’s role.

Swapping pilots: Learn from the Philippines but scale smarter.

Smart grid leadership: India’s edge in software could still set global standards for charging + grid integration.

Takeaway: India has scale, ASEAN has urgency. Unless India accelerates, it may find itself learning from ASEAN instead of leading it.

Global Context

Globally, the EV race is consolidating around four poles: China, EU, US, ASEAN+India.

China dominates adoption (>35%), infra, and supply chains.

EU leads with regulation (2035 ICE bans, 20%+ EV sales share).

The US has tech + capital (IRA subsidies), but infra is patchy.

ASEAN is agile: experimenting with swapping, setting bold targets, pulling OEMs.

India has scale and startups, but hesitates on manufacturing and policy clarity.

China sets the pace, Europe writes the rules, the US bankrolls the race, and ASEAN is now sprinting ahead as the Global South’s test bed. India must decide if it will run alongside, or watch from behind.

✍️ Conclusion

ASEAN is not a uniform market, but a patchwork of bold experiments.

🇸🇬 Singapore proves adoption accelerates with aligned policy.

🇹🇭 Thailand shows infra + industrial discipline pay off.

🇻🇳 Vietnam illustrates the power of a national champion.

🇮🇩 Indonesia leverages resources for two-wheeler scale.

🇵🇭 Philippines demonstrates regulatory boldness through swapping.

For India, the lessons are clear: policy clarity, infra reliability, and manufacturing certainty are non-negotiable. Sticking firmly with these will give India a fighting chance to secure the Global South’s EV crown.

The next article in this series will talk about battery technologies we observed at the event and the implications for Indian market. Subscribe to never miss an update.

This piece is proprietary and a property of ExpWithEVs. You may not republish, copy, edit, repost or reshare this piece without prior written confirmation from ExpWithEVs via email : priyans@expwithevs.in

|

|