Charging Infra QonQ - Part 1

2503 vs 2412 - Count, Average Power

Edit : Jul 2025 : If you are looking for the latest edition of EV Charging Infrastructure Reports, then please follow these links :

ExpWithEVs Products and Services

Today, we will compare the December 2024 and March 2025 snapshots of electric vehicle charging infrastructure over fifteen charts. This analysis will examine the growth and decline of CCS2 and Type 2 chargers across Charge Point Operators (CPOs) and states. We will also evaluate the average power rating of CCS2 chargers across CPOs and states. Additionally, we will identify compelling trends and insights to explore further.

Housekeeping

We have our GSTN! That was much faster than anticipated :)

Fret not, the subscription pricing isn’t going up. Going forward, annual subscribers can request a GSTN invoice for the premium subscription.

Last week, we wrote about Glida’s CCS2 jodi chargers in North India. As a premium subscriber, you can get access to any jodi chargers right away.

We are inviting journalists, data analysts, policy makers, industry insiders, customers to pitch a story at ExpWithEVs. You’ll be compensated for your time and efforts. You need not be a professional writer to pitch a story. Here’s the form with all the details! P.S. : We’ve already commissioned our first story!

Here are some of our industry-first charger intelligence tools.

2503 EVInfraBI - the deep dive into charging infrastructure in India

2503 EVTrendsBI - understand trends of growth across EV infrastructure in India. There’s also an 2503 Executive Summary pdf version which you can get your hands on right away.

2503 EVHardwareBI - this deep dive looks into the business of charger OEMs.

Note on Terminology and Data

In this article, we use "2412" to refer to data from December 2024 and "2503" for data up to March 2025. Our analysis compares these two snapshots of EV charging infrastructure, focusing on the 41 Charge Point Operators (CPOs) common to both periods. Note that the 2503 snapshot includes 49 CPOs, while 2412 includes 41. To ensure consistency, we analyze only the 41 CPOs present in both cycles. Some figures may differ from previously published reports due to this refined scope.

Introduction

This article is part of a three-part series analyzing quarter-by-quarter (2503 vs 2412) growth in EV charging infrastructure. We will cover charger counts, average power ratings, pricing trends, amenities near chargers, host types, coverage along national highways, and a special feature page across the three parts. For immediate access to the full analysis, purchase our standalone 2503 vs 2412 PowerBI report today. Annual premium subscriber benefit are additional licenses and a discounted price!

Existing annual EVTrendsBI and annual EVInfraBI subscribers will receive this PowerBI for free later this week. They will continue to receive updates for quarter on quarter analysis in sync with the scheduled data update.

Let’s dive in

CCS2 count by CPOs

Public players like BPCL, IOCL and HPCL contributed significantly to increase in public charging infrastructure. Evolute Surat hasn’t added chargers.

GMVN/Statiq added one charger and KSEB/chargeMOD removed 30% of their CCS2 network.

How are private players faring?

Among private players, ChargeZone has achieved over 20% growth from a relatively high base of installed chargers.

Glida added approximately 10% more chargers in three months, starting from a relatively high base.

Shell Recharge experienced a roughly 20% decline in reported chargers due to a mislabeling of Shell chargers on chargeMOD app. Previously, they marked "Coming Soon" chargers as "Unavailable", allowing us to count them. This issue between Shell Recharge and chargeMOD teams now appears resolved. Read how we collect our data here.

I’ve classified the CPOs in various buckets of growth and degrowth for Premium subscribers in the Annexure at the end of this article.

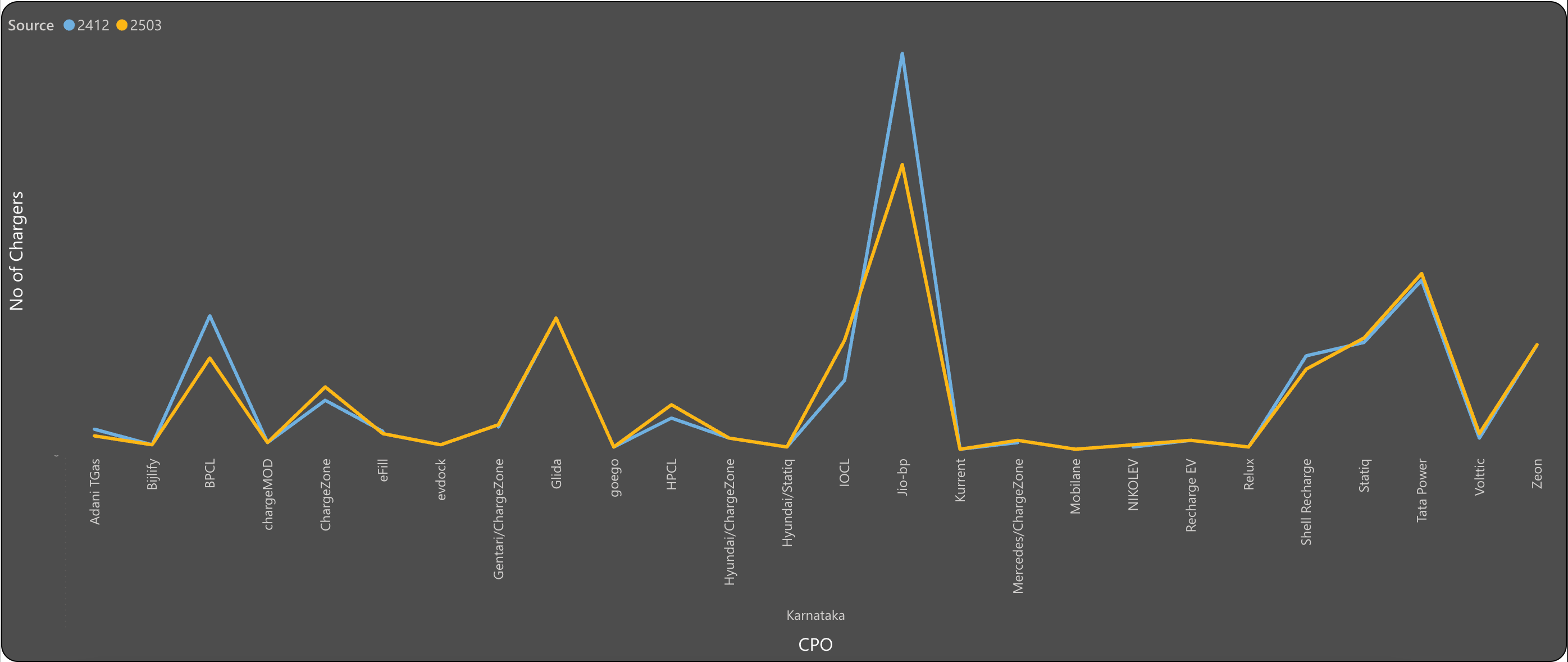

CCS2 count by States

All major states, except Karnataka, have reported an increase in CCS2 charger installations. Karnataka, however, experienced a decline of more than 5% in its CCS2 charger count. Detailed chart breakdown bucketing the states in growth and degrowth categories is present in the Annexure at the end for premium subscribers.

Maharashtra, the leading state, saw a robust growth of over 12% in CCS2 chargers. Andhra Pradesh recorded a remarkable increase of more than 30% in its CCS2 charger installations.

Let’s examine Andhra Pradesh and Karnataka in greater detail.

BPCL has significantly increased their presence in Andhra Pradesh, followed by IOCL and HPCL. Among the private players, only ChargeZone and Jio-bp have shown decent growth. Still their numbers are dwarfed when it comes to Tata Power, IOCL or BPCL.

Hyundai/Statiq broke ground in Andhra Pradesh and now has a presence!

What is the reason for decline in Karnataka?

Jio-bp has reduced its publicly available CCS2 chargers by over 35%, primarily due to the reallocation of chargers in hubs, likely now dedicated to fleet / captive operations. No major reduction has been observed in their highway charger network.

BPCL has also experienced a decline in available CCS2 chargers by over 30%, though the reasons for this are unclear. If you have insights into this, please share your comments.

In contrast, IOCL, ChargeZone, and HPCL have each expanded their CCS2 charger networks in Karnataka by at least 25%.

Type2 count by CPOs

Public CPOs

Type2 has been a contrast with CCS2 count for Public CPOs. Here, there are no significant additions. Infact, HPCL saw a drastic reduction in Type2 chargers. They’ve removed almost all Type2 chargers from their app as of March 2025. KSEB/chargeMOD and BPCL too removed Type2 chargers. IOCL and GMVN/Statiq have added Type2 chargers.

Private CPOs

The top two players, Tata Power and Jio-bp, have experienced a decline in their charger networks, with Jio-bp seeing a more significant reduction of over 10%.

Meanwhile, Zeon has expanded its Type 2 charger network by 15% from a healthy base. ChargeZone has achieved a remarkable increase of approximately 150% in its Type 2 chargers, while Bijlify has boosted its Type 2 charger count by about 65%.

The Adani TGas app previously listed private chargers as publicly accessible. This error has been corrected by Adani, resulting in a reported decline of over 20% in Type 2 charger count.

I’ve classified the CPOs in various buckets of growth and degrowth for Premium subscribers in the Annexure at the end of this article.

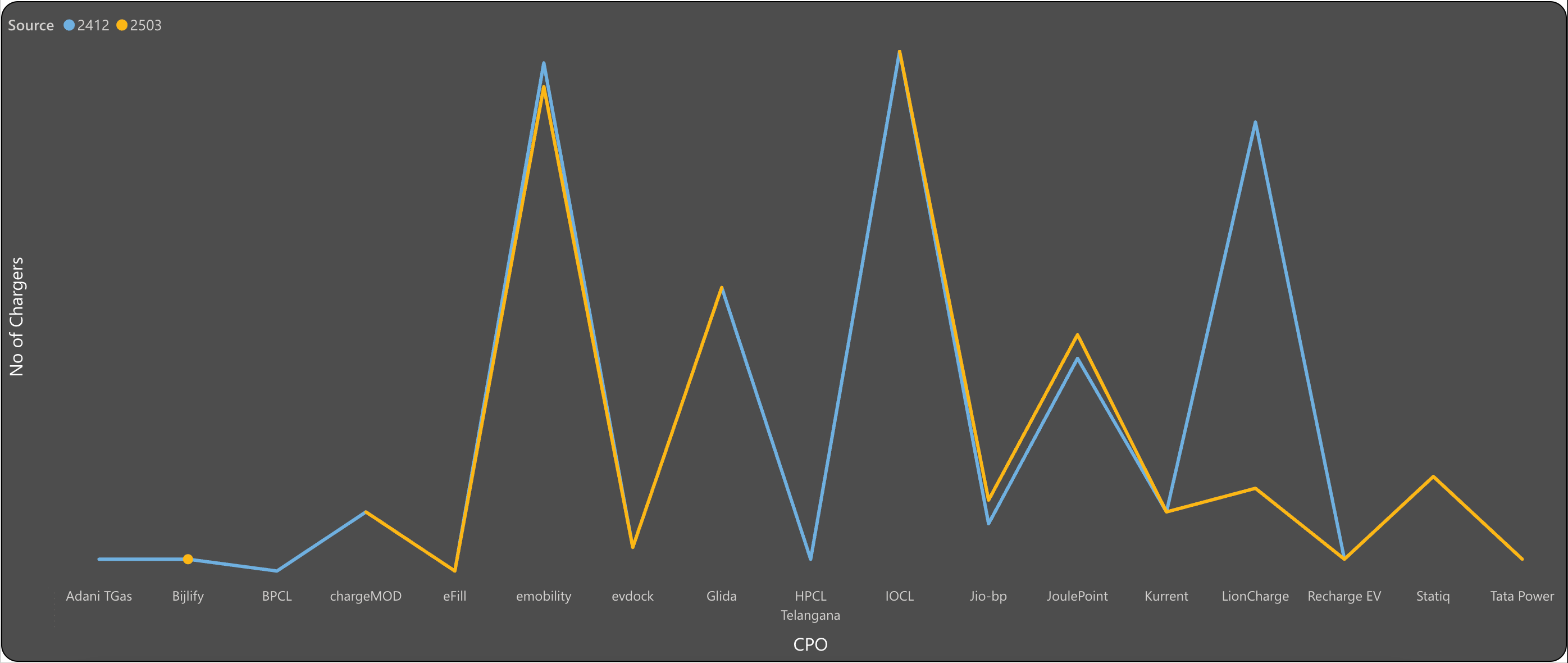

Type2 count by States

Maharashtra is the only major state to show growth in Type2 chargers, followed by West Bengal. Rest of the major states have shown some decline, most notably Telangana.

Let’s take a look at West Bengal and Telangana closely.

West Bengal has shown notable trends in charger deployment. Growth in Type 2 chargers has been driven primarily by goego and Tata Power, while other charge point operators (CPOs) such as HPCL and Jio-bp have reduced their Type 2 charger presence in the state.

In Q1 CY25, goego established its first public Type 2 chargers in West Bengal. Tata Power, meanwhile, expanded its Type 2 charger network by over 10%.

In Telangana, the picture is as follows.

LionCharge, previously the third-ranked Type 2 charge point operator (CPO) in Telangana, has significantly reduced its available Type 2 chargers, contributing to an overall decline in the state’s Type 2 charger count. Emobility has also experienced a slight reduction in its Type 2 chargers. Meanwhile, Adani TGas, BPCL, and HPCL no longer maintain a Type 2 charger presence in Telangana.

We will now examine the average power of CCS2 chargers across Indian states and CPOs. Trust me, you’re not prepared for these insights!

Premium subscribers can skip to Average CCS2 Power section directly.

If you’d like to lay your hands on these insights (and more coming over the next two articles), there are two ways to do it. Standalone one-time PowerBI (2503 vs 2412) or get an EVTrendsBI annual subscription (2503, 2506, 2509 and 2512). Links are available at the top of the article.

Stay tuned for Part 2 where we will cover Host type, amenities around chargers and the average price of charging.

Disclosures

[2023] - I had conducted a 3rd party audit of Glida's charging network and was paid for it.

[2023] - Charge Mod, EVOK, TataEV, Ador Digatron have paid for my travel to attend their events.

License and agreement

This intelligence tool is intended for the authorized buyer / organization only.

Distributing this tool or the outputs from this tool in any form outside the authorized buyers is not permitted and will be considered copyright infringement.

The data from here and this article cannot be repackaged or sold without explicit written permission of ExpWithEVs.

All rights reserved with Priyans Murarka @ ExpWithEVs.

|

|